by André Petheram, Isak Nti Asare and Richard Stirling

Why 2020 shows us that we need ‘automation resilience’

In the wake of the huge job losses caused by the coronavirus pandemic, as consumers stayed at home and demand collapsed, workers face another threat: automation [1]. In March, EY reported that, of over 2,900 corporate leaders surveyed, 36% were intensifying the process of automating their operations, with lockdowns effectively pausing production, and thereby ‘expos[ing] vulnerabilities in many companies’ supply chains.’ According to Forrester, many companies will prioritise automating jobs after the pandemic, rather than re-hiring staff.

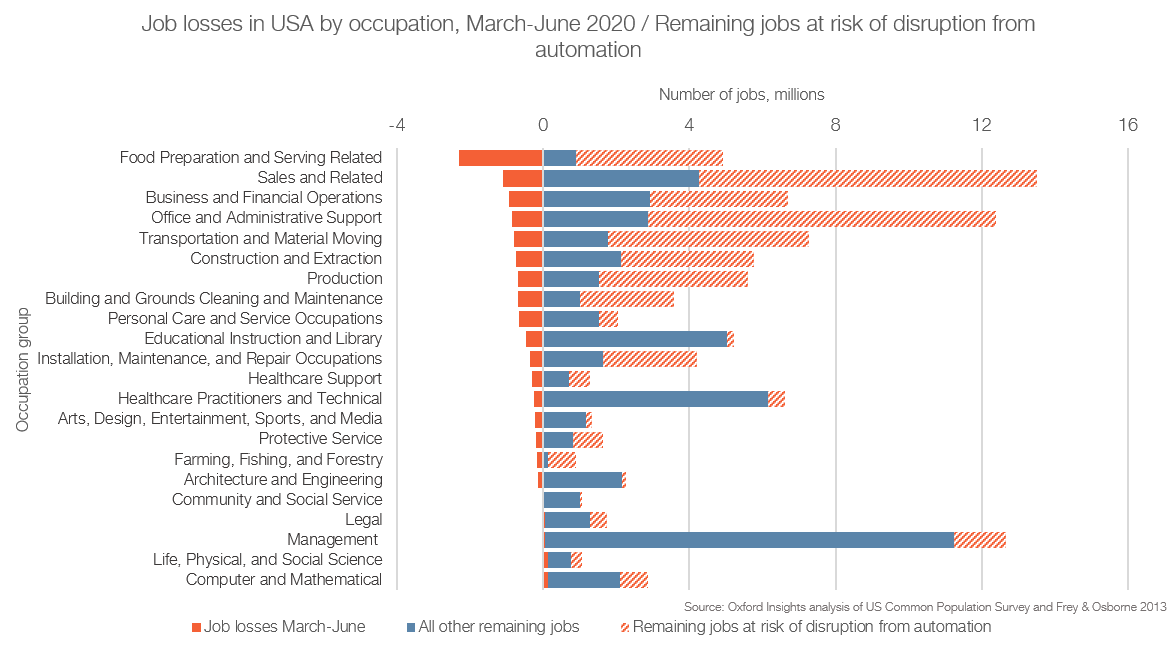

Chart 1

With workers having to stay at home to prevent the virus spreading in offices or warehouses, and jobs relying on face-to-face interaction becoming potentially dangerous, cutting out the human element begins to look like a sound investment. Businesses’ cashflows have also been severely disrupted, meaning that cutting the costs of space becomes potentially attractive, where automated systems might have a smaller property footprint than people.

But how might this break down by sector? How do jobs at risk of being disrupted by automation correlate with those impacted by the pandemic?

We looked at employment data from the US Census Bureau’s Common Population Survey, and mapped it against Frey and Osborne’s 2013 analysis of what proportion of tasks within a job can be ‘computerised’ by current technology. We found that the sectors worst affected by coronavirus unemployment include some of the sectors that are most at risk of being disrupted by future automation.

Let’s start with changes in the number of people employed in certain occupations in the USA between March and June 2020 (see Chart 1). Jobs in services have been especially badly affected, with a huge hit to hospitality and restaurant jobs.

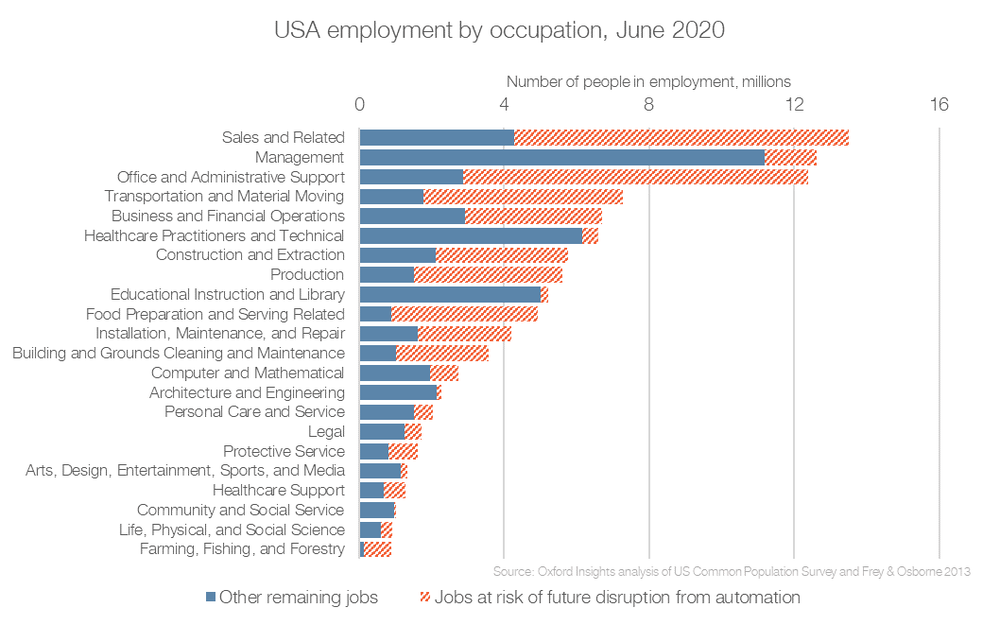

Chart 2

Of the people remaining in work (see Chart 2), the most common occupations tend to be the ones that are also most vulnerable to future disruptions from automation (with the exceptions of Management, Education and Healthcare occupations).

We calculate this by simply multiplying each individual occupation’s ‘probability of computerisation’, as estimated by Frey & Osborne, by the number of people employed in that occupation, and then aggregating the total jobs at risk by occupation group. For example, ‘Telemarketers’, within the ‘Sales and Related’ occupation group has a computerisation probability of 0.99; there are 54,756 telemarketers employed in June 2020; there are therefore 54,208.4 telemarketing jobs at risk of future disruption from automation [2].

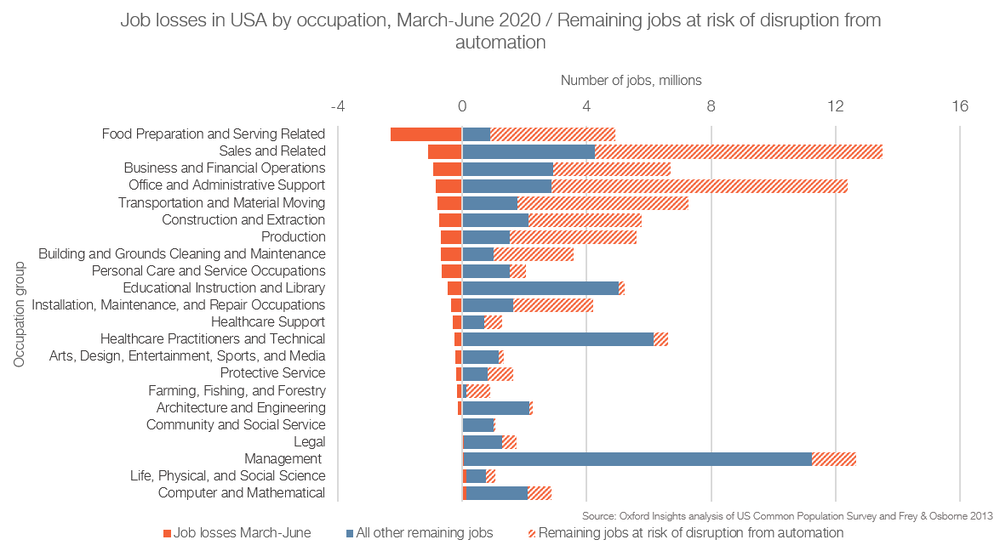

How do March-June 2020 job losses map against current jobs and future automation risk (see Chart 3)?

Chart 3

Not only are ‘Food Preparation and Serving Related’ jobs the worst already affected by coronavirus, but 82% of the remaining jobs also stand to be disrupted by automation. In the largest occupation group by number of people currently employed, ‘Sales and Related’, jobs decreased by over a million during the coronavirus pandemic, and over 9 million remaining jobs are at risk of disruption. Services are clearly badly affected by both coronavirus and possible automation, but Transportation, Construction/Extraction and Production also show vulnerabilities.

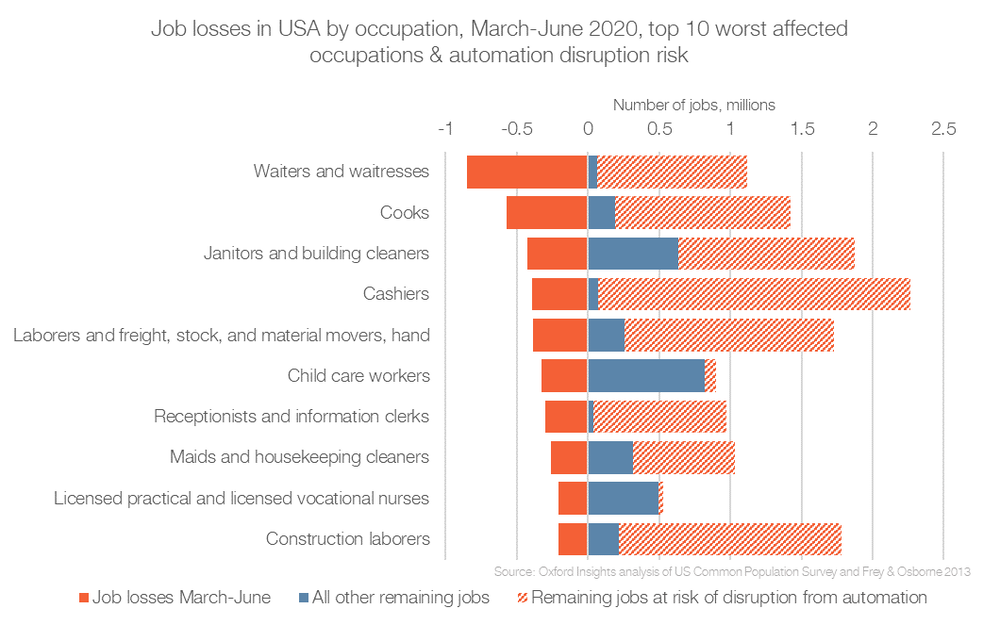

Chart 4

We can further break this down to the level of individual occupations (see Chart 4). Within the top 10 occupations worst affected by coronavirus, some (‘Waiters/Waitresses’; ‘Cashiers’; ‘Receptionists and information clerks’) see levels of future automation disruption risk of above 90%.

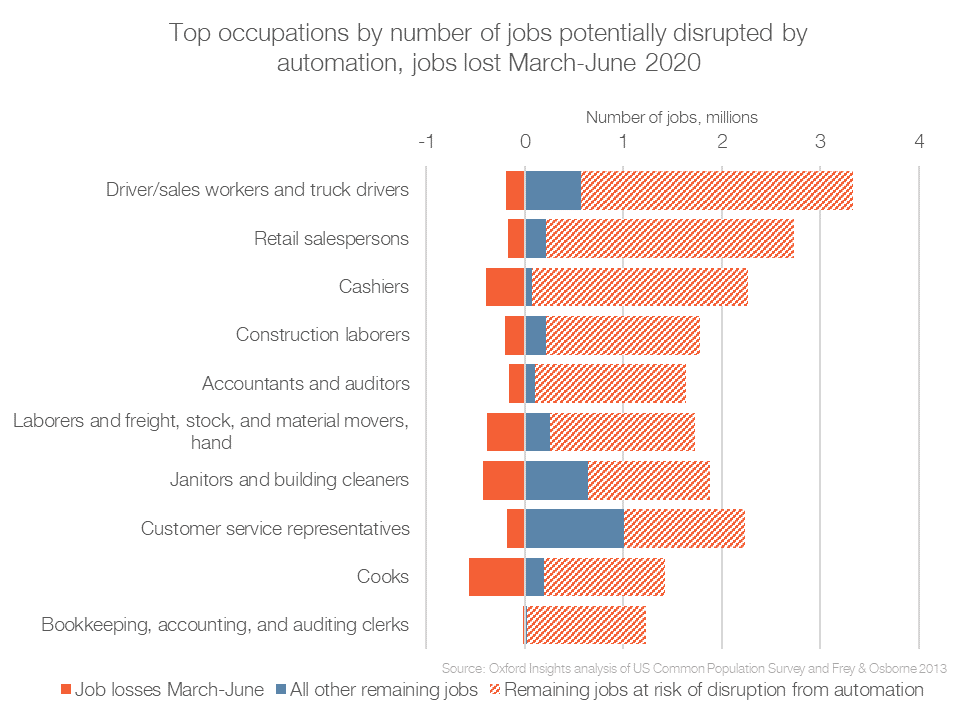

Some occupations are both the worst affected in terms of jobs lost during the coronavirus pandemic and in terms of future possible automation disruption: ‘Cashiers’, ‘Construction laborers’ and ‘Cooks’ (see Chart 5).

Chart 5

Frey and Osborne concluded that ‘as technology races ahead, low-skill workers will reallocate to tasks that are non-susceptible to computerisation – i.e., tasks requiring creative and social intelligence.’ ‘Social intelligence’ is what we have previously called a ‘human speciality’: ‘those skills at which people outperform machines [. . .and which] seem particularly close to our humanity, like emotional intelligence, creativity, and collaboration.’

Where we previously argued that human specialties offered people a competitive advantage against automated systems, the coronavirus pandemic has shown how vulnerable these specialities are. In the context of an in-person interaction, where face-to-face interaction would previously open a space to demonstrate empathy, understanding and sociality, a global pandemic makes that space a threat to people’s health. Indeed, this may emphasise the importance of developing human specialities that can be deployed remotely: a crucial potential consideration for those designing future curriculums and training schemes.

As this suggests, in the post-pandemic world we need to carefully consider the skills and economic conditions that feed into automation resilience: a labour market’s ‘ability to absorb and adapt to the potentially disruptive impact of automation’ on jobs. At a minimum, we think that automation resilience includes: workers having skills that can be quickly transferred between occupations; easy access to forward-looking retraining and re-skilling programmes; strong systems of economic and social support. As trialled in various places across the world, including the City of Stockton, California, universal basic income is possibly a crucial component of the latter. But there will be many other factors in the makeup of automation resilience that we have not yet been able to uncover.

Governments that are thinking about how to stimulate economic recovery from the coronavirus pandemic must not make the mistake of thinking that this will be a simple return to the old world. The future will contain further shocks. We need to prepare for the possibility that automation is the next one.

Footnotes:

[1] There is also the possibility that coronavirus is exacerbating an existing trend, of course. Acemoglu and Restrepo propose that the introduction of robots into US industries has implied a resultant drop in jobs, though this has been relatively small overall, at an estimated 400,000 jobs. Jobs may be being displaced in specific industries rather than on aggregate as well; with some people pointing to examples of companies using new technologies to replace administrative and executive assistants. Supermarket checkout assistants would seem to be another example. Others have questioned the impact of automation on the labour market altogether. For simplicity’s sake, our method in this blog assumes the future effect of automation on jobs, with ‘today’ as a starting-point.

[2] This method is flawed for various reasons; nevertheless, we find it a useful initial guide to the broad distribution of automation risk within different countries’ economies.